Financial Education

Posted on - 27th July, 2020 Posted by - Yallaschools

10 things I wish I knew about money when I was younger

10 things I wish I knew about money when I was younger

Hindsight is a true gift. A lot of us look back to our early years and wish we’d done things a little differently. Particularly, the way we managed our finances. This could be because many of us might not have had access to the right information. We’ve put together a list of important things we all wish we’d known earlier:

To summarise, aim to be financially independent. Try to be free from debt and seek a professional’s guidance if you need it. You don’t need to be a millionaire to have a financial plan.

xxxx

Financial Education

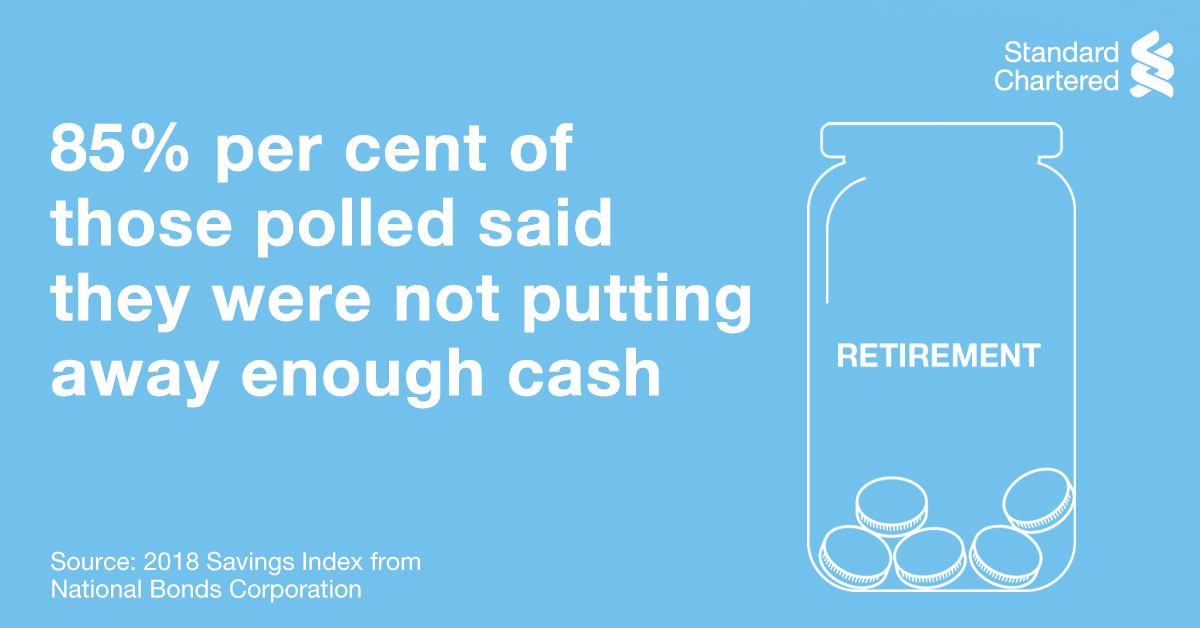

Saving For Retirement Starts Yesterday

Posted on - 18th November, 2020

Saving for retirement starts yesterday Here’s a wake-up call if you ever needed one. According to the 2018 Savings Index from National Bonds....

Financial Education

Make a confident step into your first home

Posted on - 6th October, 2020

Make a confident step into your first home There is a great sense of achievement when you buy your first home. You finally find one that fits your....

Financial Education

Paying for Tomorrow's Education Starts Today

Posted on - 17th August, 2020

Have you realised how funding a child’s education ends up teaching the parent a lesson in finance management? It begins with primary and secondary....

Financial Education

10 things I wish I knew about money when I was younger

Posted on - 27th July, 2020

.jpg)

10 things I wish I knew about money when I was younger Hindsight is a true gift. A lot of us look back to our early years and wish we’d done....

Financial Education

In An Emergency Use An Emergency Fund

Posted on - 9th June, 2020

If there’s one thing this period has taught us is that nothing is certain…especially one’s income. That’s why an emergency fund is....

Financial Education

Don’t Be A Victim, Watch out for Fraudsters

Posted on - 7th June, 2020

Don’t Be A Victim, Watch out for Fraudsters Cyber criminals are all around us, lurking in silence trying to steal your money and information. You....

Financial Education

Why everyone should have insurance?

Posted on - 19th May, 2020

People have car insurance, home insurance, travel insurance… but life insurance? Fact: Life is unpredictable. But we often ignore this,....

Financial Education

Schooling kids in money matters

Posted on - 8th March, 2020

We get it, school is expensive. And we are not even talking about school fees, extra-curriculars or after-school tuitions. We mean the daily expenses....

.png)

1.png)

9th June, 2024 at 10:45 AM

10th India Middle East Education Awards 2024 | Grand Awards

Yallaschools.com

7th February, 2025 at 9:00 AM

International Career Counselors Conference and Awards 2025

Yallaschools.com

Venue: Dubai - UAE

Amazing Career Counselor Awards

26th June, 2024

The Indian Curriculum Career Counselor Awards 2024 - Yearbook

Amazing Career Counselor Awards

18th June, 2024

Academic Excellence Awards

Academic Excellence Awards

.jpg)

26th December, 2023

4th International Middle East 'AS Level' Education Grand Awards 2023

Academic Excellence Awards

.jpg)

Latest News

.jpg) UAE

UAE Oman

Oman Bahrain

Bahrain KSA

KSA

Leave Your views & comments here

View More View Less